What are the UK laws on anti-money laundering?

Anti-Money Laundering (AML) laws are implemented to require businesses and financial institutions to follow a number of AML processes. AML regulations tackle not only money laundering but also: tax evasion, drug trafficking, political corruption and the sale of illegal goods. These laws include:

Your organisation’s legal responsibilities

Industries such as financial institutions, the hospitality sector and retail services are most at risk for money laundering and terrorist financing, so should take extra care when going through their AML checks, but it should go without saying that every organisation has a legal responsibility to adhere to the law in a number of different ways.

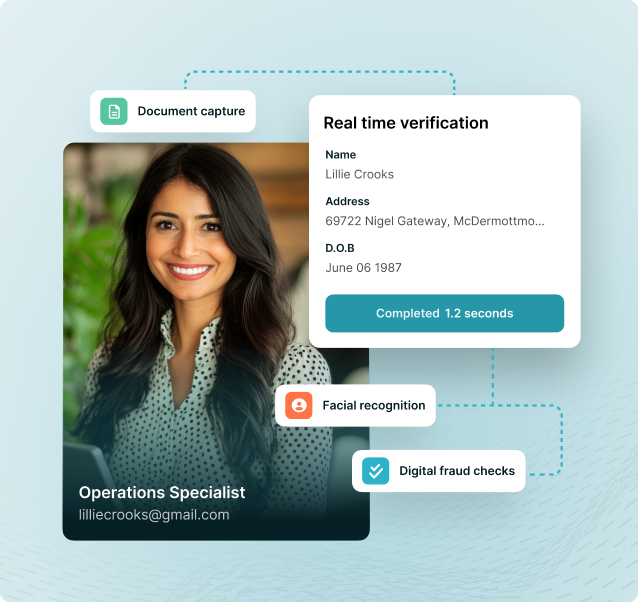

See it in action

Let one of our highly-trained sales team demonstrate the multi-award winning SmartSearch AML product.

/SmartSearch_OfficeLifestyle_Feb25_101.jpg?width=950&height=950&name=SmartSearch_OfficeLifestyle_Feb25_101.jpg)

When is enhanced Customer Due Diligence required?

Some changes to the customer’s risk might require you to undertake Enhanced Due Diligence, while others — like the customer becoming sanctioned — could force you to terminate your contract with them.

Other changes include whether the transaction or business relationship will involve:

-

An individual established in a third country where the money laundering risk is high

-

A Politically Exposed Person (PEP)

-

A close relative or known associate of a PEP

The help you need, when you need it

Whether you’re a small business just getting to grips with AML regulations or a large corporation with plenty of experience in compliance, SmartSearch can help you to comply with regulations, fight financial crime and grow your business with confidence.

-

Resource library

Explore our resource library for expert guides and tools to support your compliance processes.

-

Blogs

Discover our latest blog posts for expert tips, features, industry trends and more.

-